The day the yield curve inverted, on Wednesday, August 14th, stocks plunged and financial headlines turned grim.

Should you worry? Or is the yield curve inversion the financial fakeout of 2019?

"Longer-term rates below shorter term rates are a clear signal from bond investors that they think the United States economy is on the downswing," reported The New York Times' senior economics correspondent, Neil Irwin, "that its future looks worse than its present." But this widely-reported storyline in the financial press misses important context.

In the past, when the yield curve inverted, it was usually because investors saw fundamental economic measures deteriorating, but that's not happening now. Rear view mirror investing — assuming history will repeat itself — is not smart in current conditions, because unprecedented negative yields in Europe and Japan make the road ahead different this time.

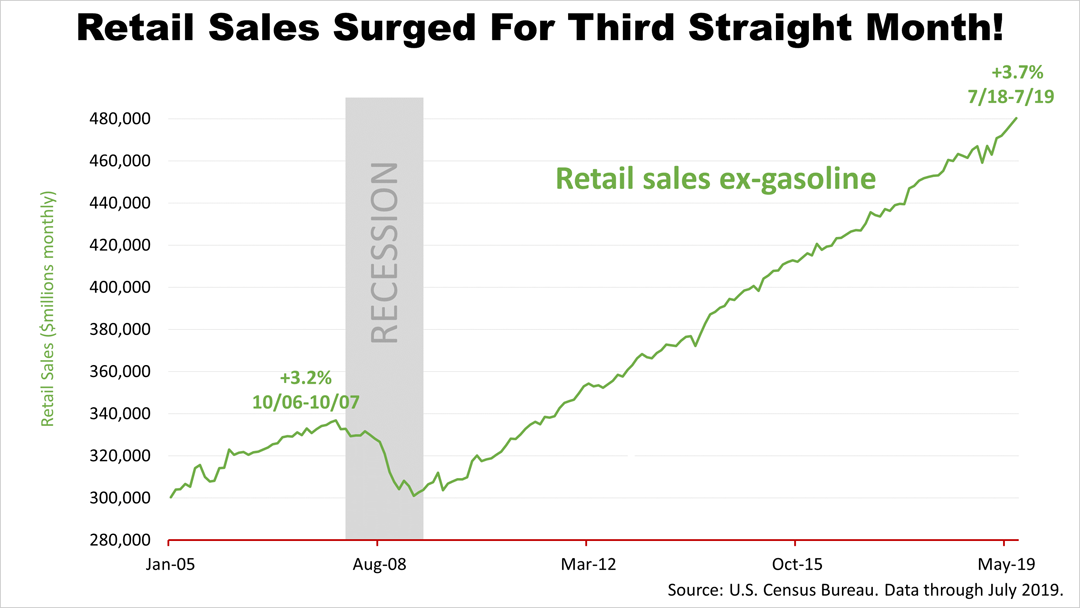

At the same time stocks plunged on recession fears triggered by the yield curve inversion, the retail sales report from the U.S. Census Bureau in the 12 months through July surged 3.7%! That followed a 3.8% spike in June and a 3.1% rise in May. Since 70% of U.S. economic activity is consumer driven, the continued strength in retail sales extinguished recession fears. When consumers are spending like this, a recession cannot be unfolding.

The retail numbers are part of a growing body of evidence that the yield curve may be making a recession look much closer than it actually is. It's a broken indicator.

This doesn't mean the yield curve is not a useful forecasting tool. It just means it's not a useful tool in the current economic situation. A hammer can't fix every problem.

And things really are different this time because the current inversion of the yield is caused by an unprecedented condition: Negative yields in Europe and Japan, which are depressing yields on long-term U.S. bonds!

From a prudent professional's perspective, the inversion is a technical market problem of supply and demand and not a "real" economic problem. It's wise to plan on your retirement portfolio's fixed-income allocations yielding lower returns in the years ahead, but that doesn't mean the U.S. is headed for a recession. Fears about the inversion of the yield curve heightened stock market volatility but that does not mean the decade-long, expansion-fueled bull market is over. It seems likely to turn out to be the financial fakeout of 2019.

This article was written by a professional financial journalist for Advisor Products and is not intended as legal or investment advice.

© 2024 Advisor Products Inc. All Rights Reserved.

Eagles' Club in LA, CA for assistance with managing your portfolio.

Eagles' Club

Administration office:

120 Encino Avenue

Camarillo, CA. 93010

Los Angeles Office

10880 Wilshire Blvd. Suite 2222

L.A, CA. 90024

Fax: 818-992-9997

Toll Free: 866-900-AIDA

aida.eaglesclub@adviserfocus.com

Mutual of Omaha Investor Services, Inc. and its representatives do not provide tax or legal advice. Any tax or legal information provided here is merely a summary of our understanding and interpretation of some of the current regulations and is not exhaustive. Tax-law is subject to frequent change; therefore it is important to coordinate with your tax advisor for the latest IRS rulings and specific tax advice, prior to undertaking an investment plan.

Securities offered through Mutual of Omaha Investor Services, Inc. a Registered Broker/Dealer. Member FINRA/SIPC. Advisory services offered through Mutual of Omaha Investor Services, Inc., a SEC Registered Investment Advisory Firm. Eagles' Club and Mutual of Omaha Investor Services, Inc are not affiliated.

Securities, Insurance and Advisory licensed in State of California. California Department of Insurance License Number 0660322. Also Insurance licensed in Kentucky.

![]()